{kind=link}

If you're about to close on a new house, your timing couldn't be better. Thanks to new mortgage rules from the Consumer Financial Protection Bureau (CFPB) that kicked in on Oct. 3, 2015, there's good news on the dreaded loan paperwork front.

You'll now receive transparent loan and closing documents, which could save you money on small-print fees you might otherwise miss. In addition, you'll get these docs three days prior to closing -- not 15 minutes as sometimes happens -- before it's time to make everything official.

The downside? The new rules, nicknamed "Know Before You Owe," bring some challenges. But a REALTOR® can guide you through the paperwork and the roughly four- to six-week home closing process so you'll know what you need to provide to the lender and when. In the meantime, here's everything you need to know before you owe:

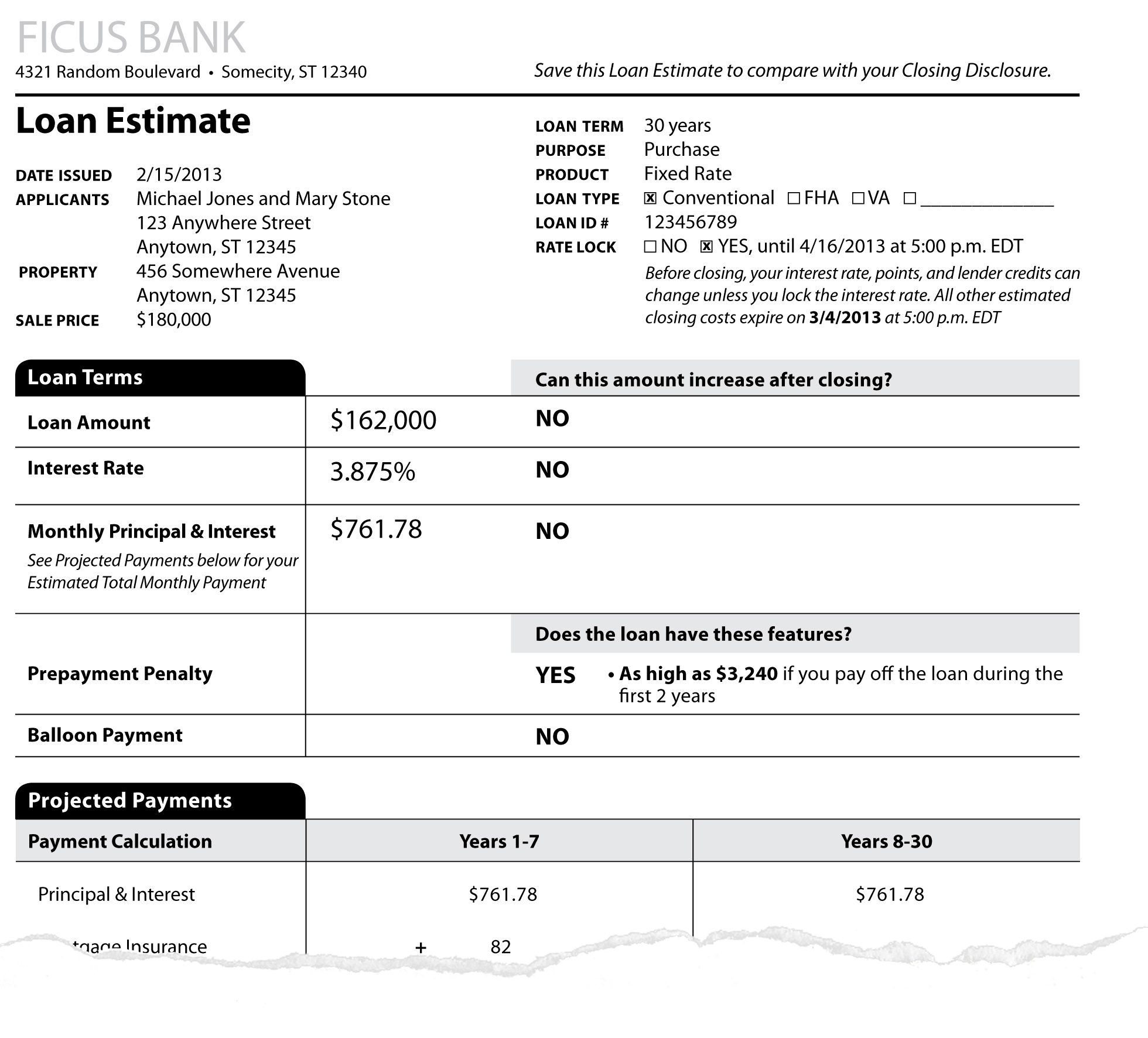

What Paperwork Will I Get? A Loan Estimate

{kind=link}

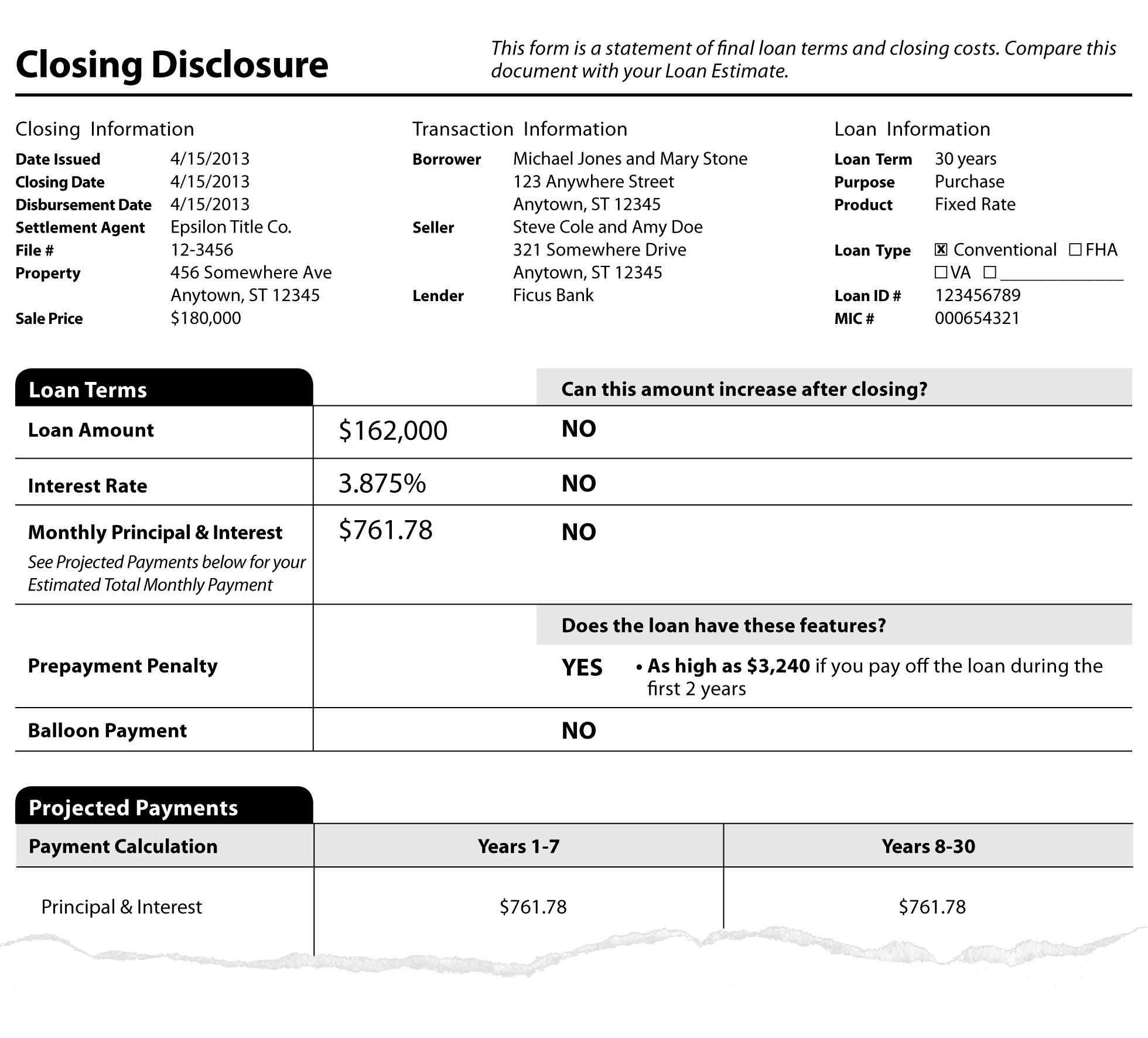

What Paperwork Will I Get? A Closing Disclosure

{kind=link}

"[The docs] give [buyers] every single bit of data tied to the purchase of that home," says Ben Niernberg, executive vice president for business operations and development at Northbrook, Ill.-based title insurance agency Proper Title. And with knowledge comes power.

How to Read the New Forms

The numbers on both the loan estimate and closing disclosure are grouped by category. Here are the highlights:

- Loan terms. You'll see the total amount of the loan, the interest rate, and the monthly payment for just the loan itself. The section will also say whether there's a penalty for paying off the mortgage ahead of time or if you're on the hook for a big balloon payment after some number of years. (You don't want one!)

- Projected payments. This is the amount you can expect to pay every month, including the mortgage, any mortgage insurance, and estimated taxes, insurance, and assessments. The only change to your monthly nut in the future would be a property tax or insurance cost increase.

- Costs at closing. Here's where you see the total amount of cash you need to bring to closing. In the LE, it's an estimate; in the CD, it's a final number.

- Closing cost details. This breaks out all the additional fees, whether from the lender or for third-party services. In the LE, you'll see the third-party fees split into those you can price shop for and those you can't. For example, you'll have to use the lender-chosen appraiser, but you can shop around for homeowners insurance. In the CD, you'll see a final list of services you shopped for and those the lender arranged.

There are some additional differences between the LE and the CD. For example, the CD lists amounts already paid on your behalf, such as a deposit or a credit that the seller has given you to cover the cost of fixing a problem. Naturally, the lender can't know about these when preparing the LE.

Timing Is Everything

Because of the strict document timing rules the lender has to follow, it's important to provide the lender with the information it needs to process your loan promptly. Your real estate agent will help ensure that paperwork and negotiations with the seller are completed in time so there are no delays.

What could cause a snafu? Three main things. (But don't sweat them. They aren't likely to happen, according to the CFPB.)

1. The interest rate on a fixed-rate loan goes up 1/8th of a percent or the variable rate on an adjustable-rate mortgage (ARM) goes up 1/4 of a percent between the time you get the LE and CD.

2. The borrower (you) says, “Hey, I don't want an ARM after all. I want a fixed-rate loan."

3. The closing doc lists a prepayment penalty or a balloon payment that wasn't in the LE.

If one of these did occur, the three-day closing period between receipt of the CD and the closing itself would halt and need to be restarted, adding at least another three days.

Most issues, however, can be resolved at closing or up to 30 days after.

What Else Should I Know?

If you're selling and buying, talk with your agent about the wisdom of scheduling back-to-back closings and what the best timing for those might be. Same for the final walk through.

Bottom-line: The LE and CD are a good thing. "The law requires that the estimates be in good faith, so they have to be as accurate as possible," said Jobe Danganan, a former CFPB lawyer and now chief legal and compliance officer with San Francisco-based mortgage-shopping site Sindeo. If figures differ too much, the lender can be on the hook to make up the difference. Even if the difference isn't that major, you now have some time to discuss it.

Related: